From casual swipers to committed romantics, millions across the globe now turn to dating apps in pursuit of meaningful connection, and the industry built around that search has never been more lucrative. Fuelled by subscription upgrades, premium tiers, and à la carte features, promising better matches and more dates, the global dating app market has evolved into a $12.5 billion industry in 2026, supported by more than 350 million active users.

Yet love, it turns out, is not free. Studies suggest the average paying user spends around $19 per month on subscriptions and premium features, a figure that can rise sharply as many singles juggle multiple apps simultaneously in the hope of improving their chances.

As debates over the true value of digital dating intensify, and users increasingly question whether premium features genuinely deliver on their promises, the boundary between finding love and financing an algorithm has grown ever more indistinct. This inspired the team at PlayersTime to take a closer look at the real price of modern romance.

To compile this report, we analysed app download and revenue data, alongside year-on-year growth trends and available user demographic and market share figures. We also examined the current pricing, taking average price per month across the different subscription tiers into consideration (free and non-standard plans were not included). We then estimated monthly matches and applied a standard match-to-date conversion rate, adjusted for platform differences, to calculate the approximate cost per date for both men and women across each platform, revealing how much a date effectively costs even before it takes place.

Key insights:

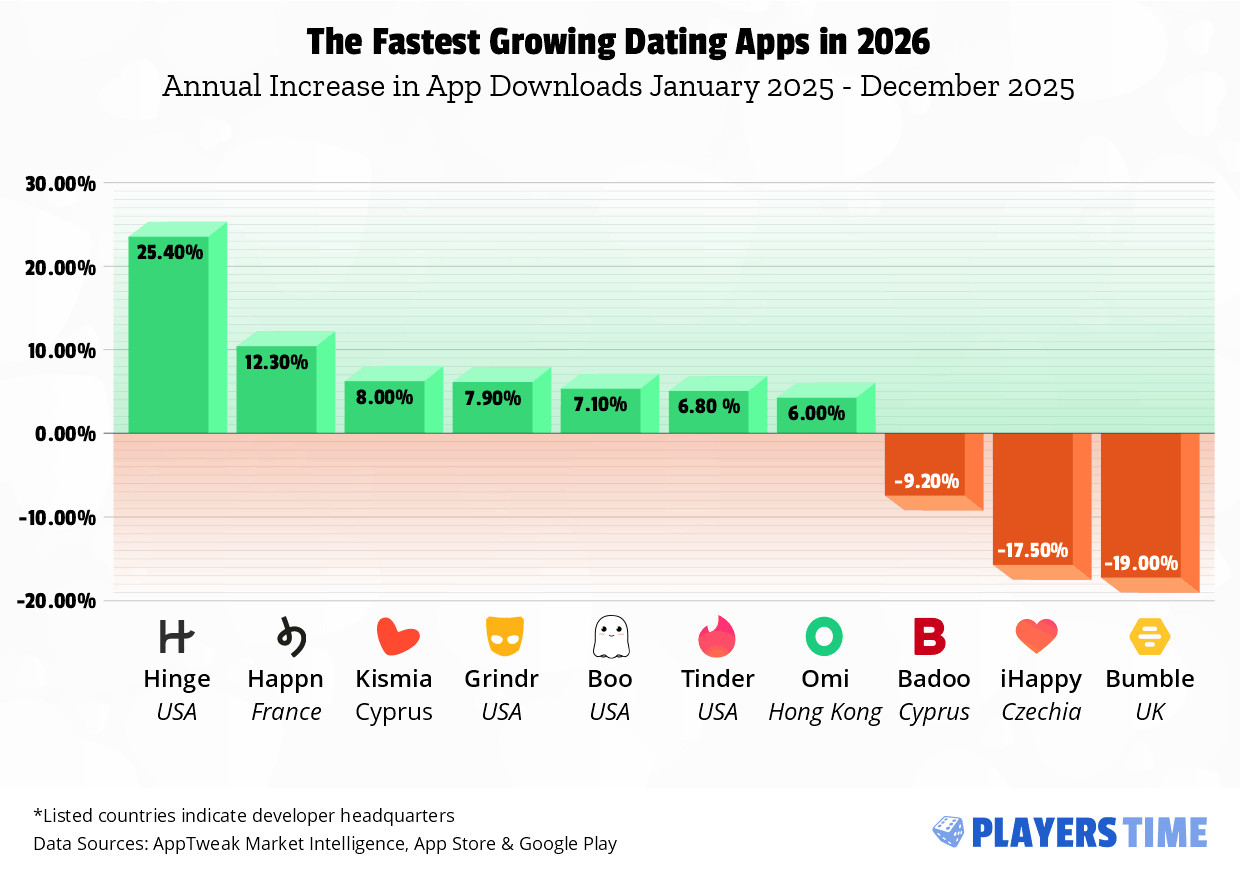

- Hinge offers the best value for money ratio in 2026, where securing a date costs an estimated $9.83 for men and $3.61 for women, based on subscription pricing. It undercuts every other platform on efficiency, while also being the fastest-growing app of 2025, recording a 25.4% YoY growth in downloads.

- Tinder Platinum represents the highest subscription ceiling on the market at $35.99 for 1 month, while Bumble Premium offers the highest average monthly pricing ($22.22) across all subscription periods.

- Men pay significantly more per date than women across all platforms, between 145% and 458% more, depending on the platform. On Bumble Premium, the cost per date is $55.55 for men versus $9.95 for women, while on Tinder Platinum, it is $19.77 for men versus $8.06 for women.

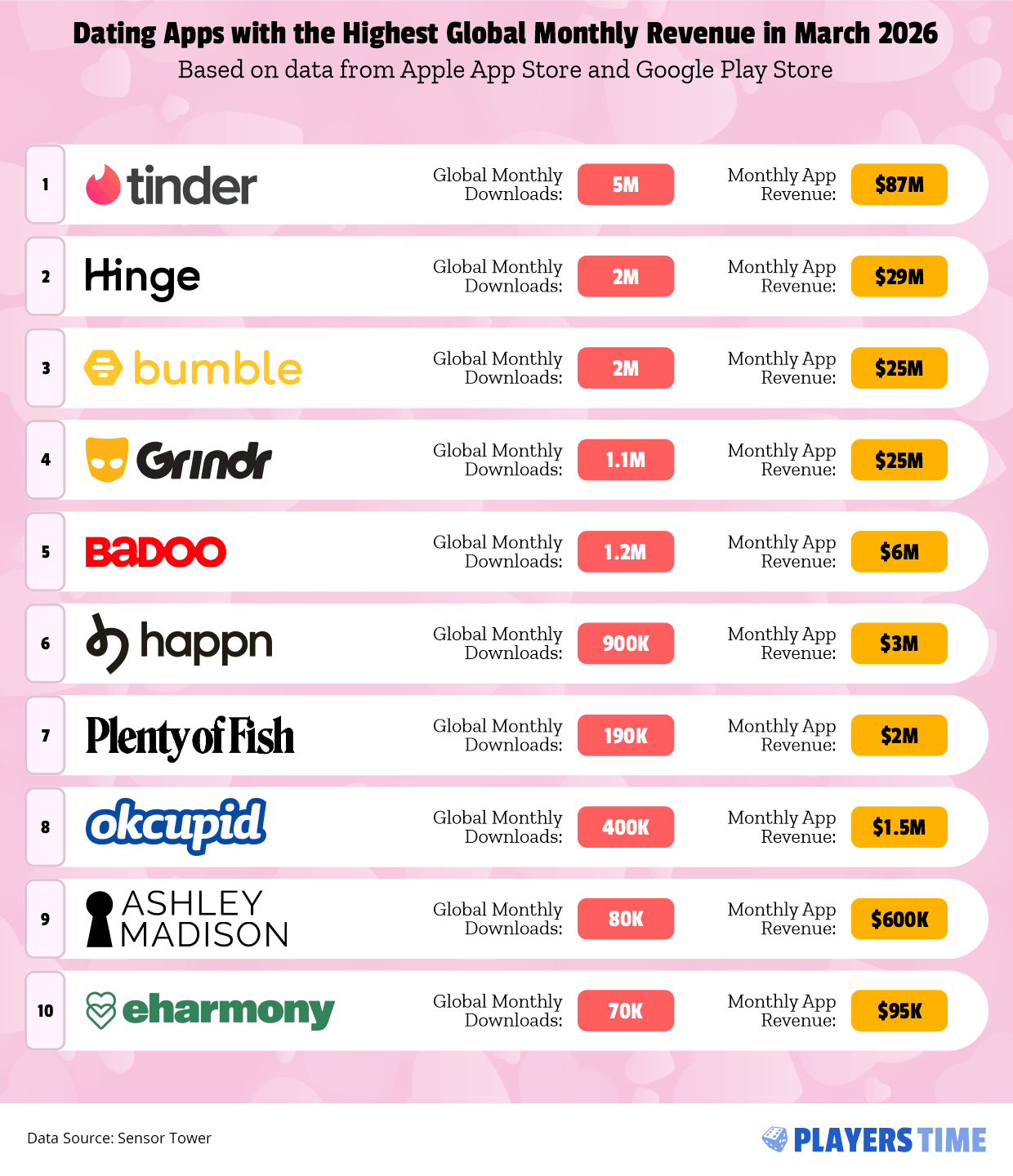

- In March 2026, Grindr nearly matched Bumble’s entire monthly revenue of $25 million, despite attracting roughly half Bumble’s number of new users. Meanwhile, Bumble is losing users with -19% YoY growth, yet continues to generate millions in revenue.

The True Cost of Swiping: A Breakdown of Dating App Pricing

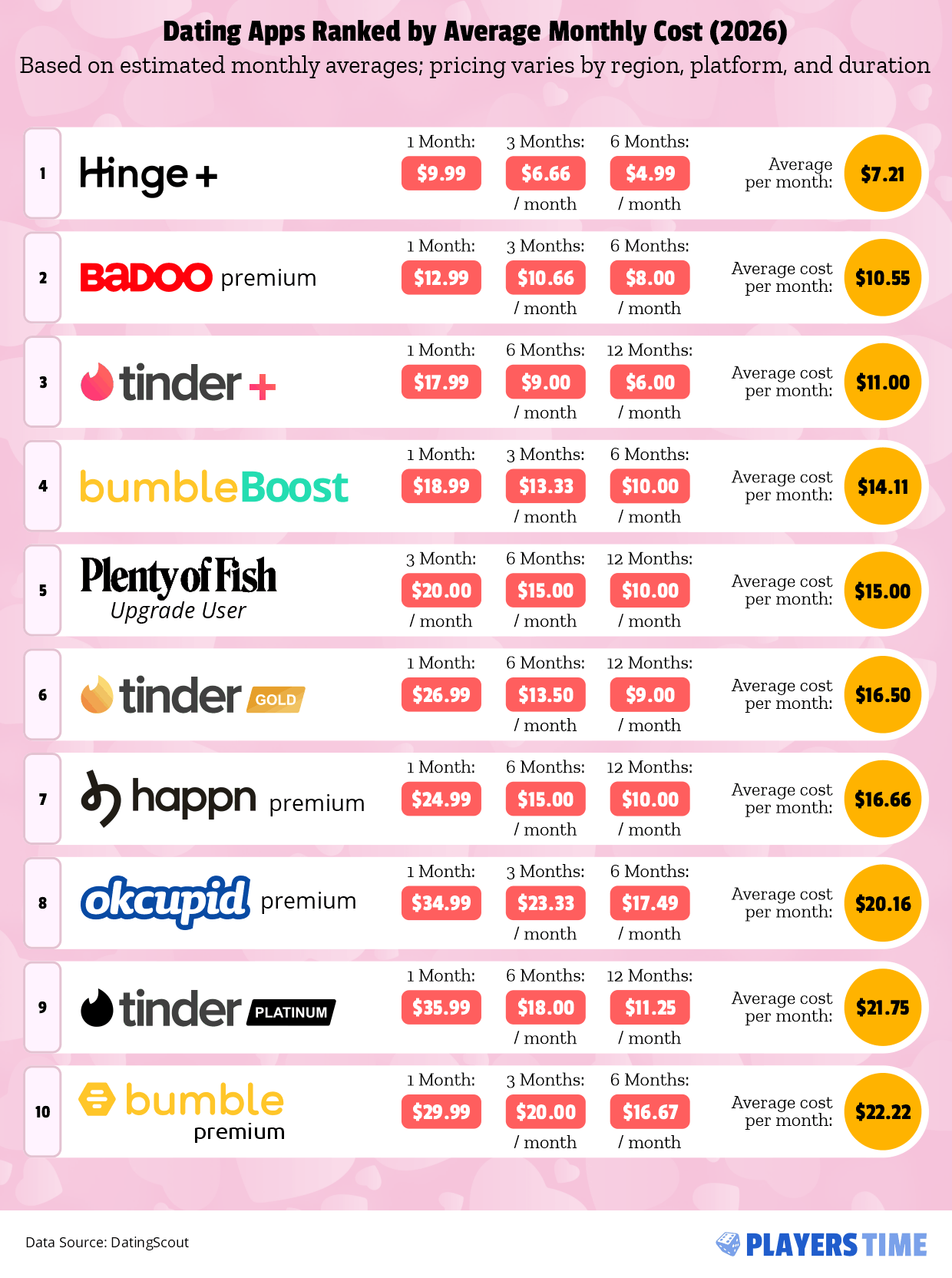

Data shows a clear three-tier pricing structure across dating apps. At the budget end, Hinge ($7.21/month) and Badoo ($10.55) stand out. Hinge is especially notable for its low cost, alongside targeting users seeking serious relationships, making it arguably the strongest value for money in the dataset. Badoo, one of the oldest platforms and popular in Europe and Latin America, uses a broader social discovery model based on interests and proximity rather than strict compatibility matching.

In the mid-market, Tinder Plus, Bumble Boost, Plenty of Fish, and Happn cluster between $11.00 and $16.66. Tinder, the world’s largest dating app by users and originator of the swipe mechanic, enters here at $11 for Plus, though it scales into higher tiers. Plenty of Fish (founded in 2003 in Canada) relies on high-volume messaging with fewer contact restrictions. Happn, a French app, matches users via real-world proximity rather than profile browsing, at $16.66.

At the premium level, Tinder Gold, OkCupid, Tinder Platinum, and Bumble Premium range from $16.50 to $22.22. Tinder’s upper tiers add features like seeing who liked you and messaging before matching, raising costs up to $21.75. OkCupid ($20.16) uses detailed questionnaires and compatibility scoring, reflecting a more analytical approach. Bumble is the most expensive at $22.22 per month on average, distinguished by women initiating first messages in heterosexual matches.

What these figures don’t capture is how quickly costs escalate beyond a flat subscription. Dating apps have become adept at monetising social validation, the very human need to know how others see us. Tinder hides the identity of users who liked your profile behind a paywall. Hinge shows likes are waiting, but reveals who sent them only to subscribers. The app knows something you don’t, and charges you to find out.

Most platforms compound this further with boosts, paid features that push profiles to the top of the queue, representing an additional and often impulsive layer of spending that can quietly double or triple the real monthly cost of using an app.

From Match to Meet

How Expensive Is It to Get a Date Using Dating Apps in 2026?

Based on average monthly matches (33 for men, 81 for women) and a 1-in-30 match-to-date rate, with adjustments for lower match rates and app limits on Bumble and Hinge (Bumble: 10-20% for women, and 3% for men; Hinge: 8 swipes/day cap)

* Prices are estimated monthly averages and vary by region, platform, age, and subscription duration.

Data Sources: Quora, DatingZest, SwipeStats, DigiExe, CatfishFinder, SwipeStats

Knowing what a subscription costs is one thing, but knowing what it actually delivers is another. To measure this, we estimated cost per date, calculated by dividing the monthly subscription price by the expected number of dates, based on match volumes and a 1-in-30 match-to-date conversion rate. You’re effectively paying that amount just for the chance to go on a date, not the date itself. In other words, users are spending anywhere from a few dollars to over $50 simply to get to the starting line, with no guarantee the other person will reply, show up, or lead to anything beyond a single meeting.

Hinge stands out as the best-value app for both men and women, with its base subscription translating to an estimated $9.83 to secure a date for men and $3.61 for women, figures that outperform every other platform in the analysis. Tinder’s three plans, by contrast, result in roughly the same estimated number of dates, meaning upgrading from Plus to Gold to Platinum mainly improves visibility rather than increasing real-world outcomes.

Across all platforms in our analysis, men consistently pay between 145% and 458% more per date than women on the same subscription, a gap that widens significantly, depending on the app. Nowhere is this more pronounced than on Bumble, where the platform’s design of women being the ones having control over initiating conversations further complicates things. A man has no ability to reach out, regardless of his subscription tier, making his cost per date entirely dependent on whether his match decides to text first. The result is a dramatic imbalance: based on our estimates, men on Bumble Premium spend around $55.55 to secure a single date, compared to just $9.95 for women, more than five times the cost for the exact same subscription plan.

The reason behind this disparity comes down to a simple numbers game. On every major platform, men significantly outnumber women, and fewer women means fewer matches, fewer conversations, and ultimately, a higher cost to land a date.

Gender Ratios Across The Most Popular Dating Apps

Revealing The Gender Imbalance

Based on latest available user demographics

Male

Female

Data Sources: Business of Apps, SSRS

When Gender Imbalance Becomes a Price Tag

The gender imbalance across major dating apps is hard to ignore, and it becomes even more striking when looking at how heavily skewed user bases are across platforms. On Tinder, approximately 75% of users are men compared to just 25% women, meaning three out of every four people competing for attention are male. Hinge narrows the gap slightly at 64% men and 36% women, while Bumble, often seen as the most balanced, still sits at 60% men and 40% women. Even on a platform designed to give women more control, they remain significantly outnumbered.

For men, these ratios don’t just influence outcomes, they fundamentally reshape the economics of participation. What appears as a fixed monthly subscription becomes a variable cost in practice, fluctuating based on how competitive attention becomes on each platform. In effect, the same price buys very different levels of opportunity depending on where you are in the market.

The Market: Who’s Winning the Dating App Wars in 2026

The revenue figures behind the apps reveal a market that cannot be understood through downloads or subscription prices alone. Tinder dominates the industry with an estimated $87 million in app revenue in March 2026 alone, almost double the combined earnings of Hinge and Bumble, its two closest rivals. This performance reflects a monetisation model where higher subscription tiers primarily increase profile visibility, exposing users to a larger pool of potential matches and raising the probability of engagement, but without guaranteeing matches, conversations, or downstream dates.

This distinction is central to much of the criticism around dating app monetisation: users are not paying for outcomes, but for improved odds within a system where success remains inherently uncertain. Despite this, Tinder’s revenue engine remains highly resilient.

The most striking figure in our analysis belongs to Grindr. With 1.1 million downloads in March 2026, it attracted fewer new users than any other major app in our ranking. Grindr still generated around $25 million in monthly revenue, matching Bumble, despite its significantly smaller inflow of new users. This suggests a deeply engaged user base, where a greater share of users convert into paying subscribers or premium features, making Grindr one of the most commercially effective dating platforms in the world on a per-user basis.

Elsewhere, the contrast between scale and revenue is equally revealing. Badoo attracted 1.2 million downloads, more than Grindr, yet generated just $6 million in revenue, suggesting that downloads alone are a poor measure of a platform’s commercial health. Meanwhile, established names like Plenty of Fish and eHarmony appear to be fading quietly, a far cry from the dominance they once commanded in the pre-swipe era of online dating.

Who’s Growing and Who’s Fading

Shifting focus to growth, Hinge is the standout performer of 2025, recording a 25.4% increase in downloads between January and December, a figure that dwarfs every other app in our analysis and cements its position as the app with the most momentum heading into 2026. Backed by Match Group, it has built its entire brand around the tagline ‘designed to be deleted’, positioning itself as the app for people who want to get off dating apps for good. Whether that promise holds is a question its $29 million in monthly revenue leaves open.

Happn, often overlooked in conversations dominated by the major three, posted a 12.3% growth rate, a notable resurgence for an app built around location-based chance encounters. Grindr and Tinder also grew, at 7.9% and 6.8%, respectively. Ranking sixth in growth, Tinder appears to be maintaining rather than expanding its dominance.

At the opposite end, several established platforms are now in decline. Badoo fell by 9.2%, while smaller competitors such as iHappy dropped by 17.5%. The most significant contraction, however, comes from Bumble, which saw a 19% decline in downloads, the steepest one in the dataset. Despite maintaining substantial revenue levels, this divergence between monetisation strength and user acquisition raises questions about the platform’s long-term growth trajectory.

The Shifting Balance of Power in the U.S. Dating App Market

According to the most recent available market share estimates for the U.S. market, Tinder and Bumble appear closely matched at first glance, holding 25% and 24% market share, respectively. Yet, recent growth trends suggest this balance may be more fragile than it appears. Tinder continues to edge forward, while Bumble is losing users, suggesting that its market share position may look very different in next year’s figures.

The Largest Dating Apps by Market Share

Based on estimated market share in the U.S.

Data Sources: Visual Capitalist

The more compelling shift is visible when looking at Hinge. With an estimated 18% market share and the strongest growth rate in the dataset, it is steadily narrowing the gap on the two market leaders, and it is not the only challenger worth watching. Hily (2017), aimed squarely at Gen Z and Millennials, already holds a 7% market share, level with the long-established Plenty of Fish (2003), suggesting that newer personality-focused platforms are already punching above their weight.

Badoo, meanwhile, sits at 4%, and like its parent company, Bumble Inc., which owns both apps, it is heading in a worrying direction. Bumble Inc. reported a revenue decline of nearly 10% in 2025, with paying users falling by more than 11% across both platforms, painting a concerning picture for a company that still holds a combined footprint across two of the most recognised names in digital dating.

Love on Subscription

Dating apps have built a billion-dollar empire on the back of human longing, monetising not just the search for connection, but also the frustration that comes with it. Subscription prices represent only the entry point – the effective cost of reaching a date is often significantly higher, and the outcomes remain uneven depending on both platform dynamics and user demographics. A 2025 survey found that 78% of users feel emotionally, mentally, or physically exhausted by the experience, and yet the money keeps flowing.

The tension is unlikely to resolve anytime soon. If anything, dating apps have established a broader commercial template that extends beyond the category itself: the most durable business model is not necessarily solving a problem outright, but maintaining users in a state of partial resolution, close enough to success to stay engaged, but not guaranteed enough to exit. The data suggests that for most users, the search continues, and for the platforms, that sustained search is precisely where the value lies.

Methodology

To compile this report, the team at PlayersTime analysed app download and revenue data from the Apple App Store and Google Play Store as of March 2026, alongside growth statistics from AppTweak Market Intelligence. Gender ratio data for Tinder, Hinge, and Bumble was drawn from the latest available figures from Business of Apps, while U.S. market share estimates were sourced from Visual Capitalist. Subscription pricing data was collected from Dating Scout to ensure comparability across platforms. Additional tiers may exist for some apps, but were not publicly available through this source at the time of research. Building on this data, we calculated estimated monthly matches and applied a standard 1-in-30 match-to-date conversion rate, a figure supported by user data and platform behaviour research, adjusted for platform-specific limitations, to approximate the cost per date for both men and women across each platform.